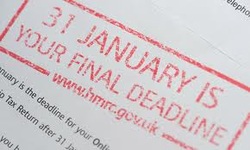

We all have to eat. That means we have to earn money one way or another and pay taxes. There are lots of different ways of working as a professional musician. For example teaching, performing, working within arts organisations, working as a session musician, writing, recording, sales through websites etc.  Often musicians may have more than one income stream to make ends meet. Its important to have more than one string to your bow - so to speak! Depending on the mix you need to think about your tax position.  Being a musician can affect your day job! Some of these may mean working as an employee - either as a musician, or in some other job while you moonlight as a musician in the evening - as the chap in the picture clearly does!. Some may involve being self employed. There are pros and cons to both. Being an employee carries various rights and responsibilities - both for employers and employees. Its fairly straight forward as an employee. Your employer will ensure that your tax and national insurance is deducted from your salary at source - i.e before you receive it. Employees get a pay slip which will set out all the payments your receive (which could be your basic salary, bonuses, commission etc), and all the deductions (e.g national insurance, tax, pension contributions).  Check your tax code Your payslip will also give your tax code. This is a number which is basically is code for the amount that you can earn before tax. Its different for different individuals depending on your tax allowances.  What are tax allowances? There are various threshholds for example, based on whether you are single, have children and are entitled to tax credits, have a company car etc. You should check this each year for your own position and ensure all the tax allowances you are entitled to are taken into account in your tax code.  A P60 Each year you will receive something called a P60. Don't glaze over - stick with it. This totals all your monthly payments and deductions and gives annual totals. Keep this. You will need it for any tax assessment. This system of deduction at source for employees is called PAYE. It simplifies tax collection for HM Treasuary and also for individuals. In addition it makes it more difficult for people to evade tax. Usually that's the end of the story for employees. But even so, if you encounter expenses which are tax deductable, these can be claimed either directly by writing to the Inland Revenue (if below £2500) or through completing a Self Assessment tax return. Things like professional memberships, spending on some work clothing (where this is required for your work) etc can be claimed. This would usually mean a change to your tax code for the following year.  If you are self employed - or if a portion of your income comes from self employment you must keep records and complete a Self assessment tax return. This will apply to you if you are a freelance musician. How do you determine whether you are self employed? There are various tests. If you make the decisions, own the assets, find your customers and are responsible (i.e legally liable if something goes wrong) then its likely that you are self employed. There are various different ways of trading which you need to make a decision about. For example, you can trade as a sole trader, partnership, or limited company (which is legally separate from the shareholders and limits any losses to the company). There are different reporting requirements and tax regimes. Most musicians won't be in the category of a limited company (which is quite complicated). But there are also advantages - the key one being that any liability is limited to the assets of the company and not personal assets - so depending on the risks - you might want to think about it. For example, if you set up a business providing stage sets, scaffolding, and equipment at large events involving high profile musicians and members of the public, go for a limited company. But if you teach a few music lessons at home - then I'd set up a sole trader - with appropriate insurance etc. There is lots advice about the advantages and disadvantages of each on the web. Try the Scottish Government's Business Gateway site which gives a lot of helpful information about starting up a business in Scotland. If you become self employed you must tell the Inland Revenue and keep records of income and expenditure. You must keep details of sales, purchase, expenses, wages, bank statements. Sales means any goods and services that you sell. Purchases means things that you might buy in the course of the business. Expenses are things that you might need to carry on your business e.g. fuel, computers, website costs, advertising. Its worth thinking about simple accounts software . It makes keeping accounts a bit easier and can also help you keep track of where the money goes.  If you work from home there is a decision about whether you claim for a portion of your bills. For example you can claim a percentage of electricity, gas, telephone, internet costs etc.  When you set up our business, I advise you to claim, claim, claim. If you start out underclaiming its more difficult to change your pattern of claiming later without a lot of hassle explaining! And remember that to claim for your expenses act it only doing what you are entitled to! If you own your home you should take advice. Claiming a portion of expenses can affect the tax status of your home. You may become liable for some capital gains tax when you sell your home - not a good trade off. Whatever your position, employed or otherwise, if you earn income (other than through your employer and the PAYE system) you must fill out a self assessment tax return. If you do this online - as I do - the deadline for submitting it and paying any tax is 31 January each year. Depending how much you earn, where you are in life and how complicated your affairs, you might consider employing an accountant. Don't glaze over here. You are all going to be millionaires right? Accountants can save you more than the cost of their fees in the long run. But its not necessary and too expensive if you are just starting out. What else do you need to know about money? Take advice when you need it but DO NOT sign up until you read the small print. And I mean independent advice. If you are not paying fees to a financial advisor the advice is not necessarily truly independent - because they are being paid out of the commission from the company providing the product. Be warned - do your own research - read as many impartial website, financial press and consumer advice. Know what the charges of any financial product are and the impact it will have in any investment or savings. Remember about compounding - charges eat into this at an absolutely alarming rate. Be sure any financial product fits your needs.  There is a very good Government backed website called the Money Advice ServiceIt is impartial and is a good place to start. In particular, it has a good budgeting tool. Handy for business and personal finance. Sometimes borrowing can be a good thing - most businesses run with some sort of loan, overdraft facility. But again check charges and conditions. Mortgages can make buying a home cheaper than renting - but be sure you can afford an increase in interest. And be clear about how you pay it off. Remember the endowment policy scandal? A whole generation (including me) were sold policies as a sure way of paying of your mortgage early - only to find out that they don't repay your mortgage at all - leaving people with a massive shortfall. If you do end up buying a house, or premises or any other large asset - always try to think at a tangent. By that I mean you need to work at finding something good value. You will rarely be able to afford your ideal - wherever you are in life. There are lots of opportunities - don't be rushed. Whenever I buy something large, I try to take it out of the market. Advertise for what you want yourself. You might be surprised at what might come your way. Don't be shy. Review all your financial affairs at least yearly. I reckon you can often save up to about £1000 a year by doing this. Move electricity, gas, insurance, telephones. mortgages and saving accounts if necessary to get the best rates. Don't be afraid to ask for discounts - its an unBritish thing to do - but it can pay dividends. Educate yourself about finance so you can make informed decisions - read sites like the BBC, HM Revenue and Customs, Paul Lewis (the BBC Moneybox correspondent). Reading the Motley Fool books were the single galvanising factor for me. I ready them after the age of forty - you should read them sooner! It doesn't have to be boring and the earlier you start the better!. I like the Alvin Hall books below - plain english.

The money you save before you reach the age of 30/40 will grow far more that the same amount saved later - because of the miracle of compounding. You might also want to consider investments. You can get tax relief for buying assets into your SIP (which is like an ISA wrapper around your personal pension).

The Musicians Union also has some helpful advice for musicians on finance and pensions insurance. Its worth knowing that membership can provide public liability insurance. Important if you teach. Dealing with tax and finance is not much fun for most of us (unless you are an accountant yourself) but you can't avoid it. Don't let it build up or you will be letting yourself in for a lot of trouble and expense later. Live long and prosper!

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Fiona Harrison

|

RSS Feed

RSS Feed